Best Greyhound Betting Sites – Bet on Greyhounds in 2026

Loading...

Betting Without the Bookmaker

A betting exchange removes the bookmaker from the equation. Instead of accepting odds set by a single operator, you trade directly with other punters. One person backs a dog to win; another lays it—effectively betting that it won’t. The exchange acts as a marketplace, matching backers with layers and taking a small commission on winning bets. No bookmaker margin. No overround in the traditional sense. Just two people on opposite sides of a bet, with the exchange sitting quietly in the middle.

For greyhound racing, exchanges offer possibilities that traditional bookmakers can’t match. You can lay a dog you think will lose—something no fixed-odds bookmaker allows you to do. You can trade positions before a race, backing at one price and laying at another to lock in a profit regardless of the outcome. You can set your own odds and wait for someone to match them, rather than accepting whatever the bookmaker offers. These capabilities shift the balance of power from the operator to the punter, at least in theory.

The reality is more nuanced. Greyhound exchange markets are thinner than horse racing or football markets, which means less liquidity, wider spreads, and the occasional inability to get matched at the price you want. Exchange betting on the dogs rewards patience and selectivity. It doesn’t suit the punter who wants instant execution at the click of a button, but it rewards the one willing to wait, watch, and trade with precision.

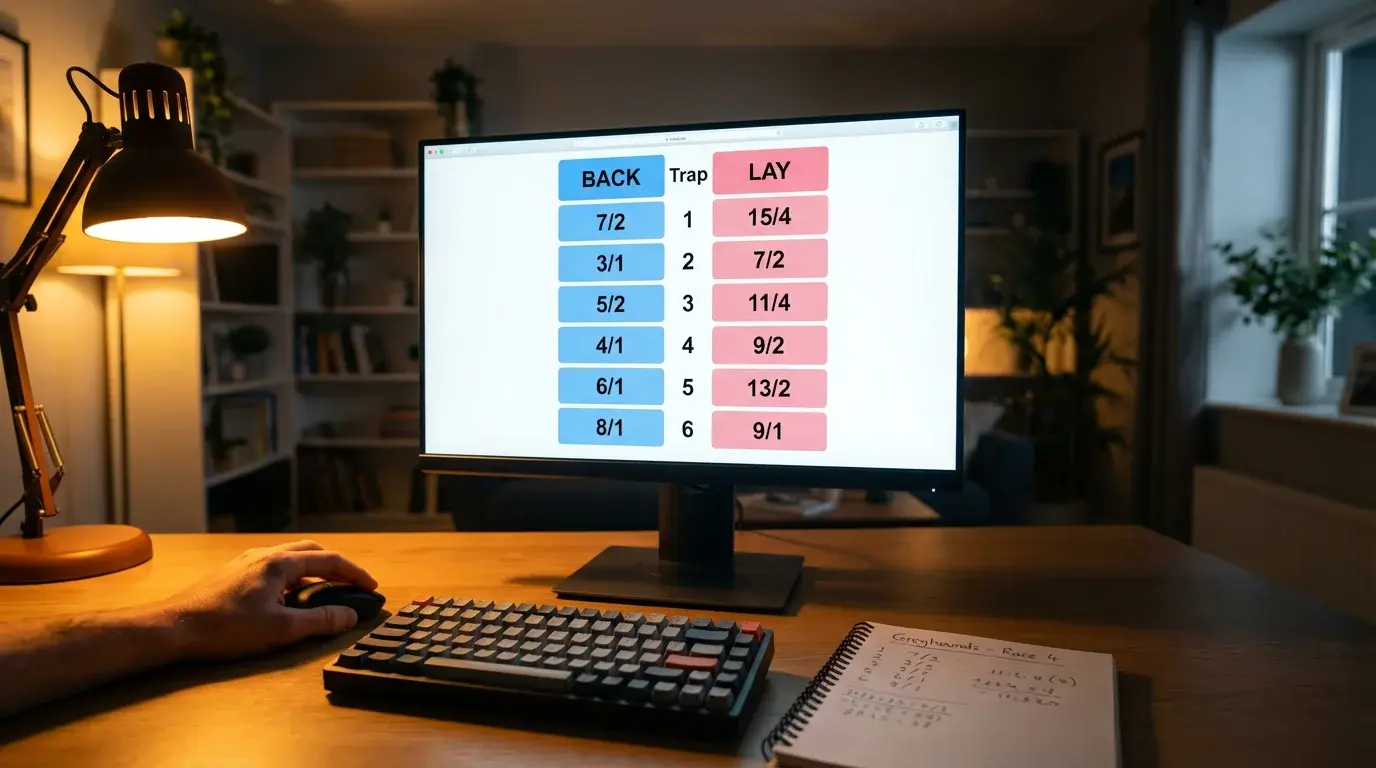

How Betting Exchanges Work

An exchange market displays two sides for every selection: the back price and the lay price. The back price is the best odds available if you want to bet on a dog winning. The lay price is the odds at which someone is willing to bet against that dog. The gap between the two—the spread—represents the market’s current state. A tight spread indicates an active, liquid market. A wide spread suggests thin interest.

When you place a back bet on an exchange, you’re offering to accept a certain price. If another user has placed a corresponding lay bet at the same price, the two bets are matched and both become live. If no matching lay bet exists, your back bet sits in the market as an unmatched offer until someone accepts it, the market moves to meet it, or the race starts and unmatched bets are cancelled.

Laying a selection means betting that it will lose. If you lay a dog at 4.0 for £10, you’re accepting £10 from the backer at those odds. If the dog loses, you keep the £10 stake. If it wins, you pay the backer £30 in profit—the £10 stake multiplied by the odds minus one. Your liability on a lay bet is always greater than the stake you accept, which is why exchange accounts require sufficient funds to cover the maximum potential payout before a lay bet is placed.

Commission is charged on net winnings, not on every bet. The standard rate varies by exchange—Betfair typically charges 5% on greyhound markets, though loyalty discounts can reduce this. Smarkets charges a flat 2% commission. This commission replaces the bookmaker’s overround as the exchange’s revenue mechanism and is generally lower than the margin embedded in fixed-odds pricing, particularly on competitive markets.

Betfair Greyhound Markets

Betfair dominates the exchange betting landscape for greyhound racing. Its greyhound section covers the full GBGB schedule, with markets opening for each meeting and individual race prices available from the morning of the fixture. The platform displays back and lay prices, amounts available at each price, and recent trading history—giving you a snapshot of market activity and sentiment.

Liquidity—the amount of money available to be matched—varies dramatically by meeting. Evening fixtures at major tracks like Romford, Monmore, and Towcester attract the most exchange activity. Prices are tighter, unmatched bets get filled faster, and the market behaves more efficiently. Afternoon BAGS meetings at smaller venues generate less interest, with thinner books and wider spreads. On a quiet Wednesday afternoon card from a secondary track, you may struggle to get a meaningful amount matched at your preferred price.

Betfair also offers a sportsbook product alongside the exchange, allowing users to take fixed odds from Betfair itself rather than trading with other punters. This dual offering means you can compare the exchange back price against the sportsbook price on the same platform and choose whichever offers better value. In practice, the exchange back price on favourites often undercuts the sportsbook price, while longer-priced selections may offer better value through the fixed-odds product where exchange liquidity is thin.

Smarkets provides a viable alternative to Betfair, with lower commission rates and a clean, modern interface. Its greyhound coverage is less comprehensive than Betfair’s and liquidity is generally lower, but for punters whose primary concern is minimising commission costs, Smarkets offers a competitive option, particularly on higher-profile meetings where both exchanges carry sufficient volume to match bets reliably.

Laying Greyhounds

The ability to lay—to bet against a selection—is the single most distinctive feature of exchange betting. In a six-runner greyhound race, laying one dog means you profit if any of the other five wins. This inverts the usual betting dynamic. Instead of needing to identify the winner, you need to identify a loser. For many punters, that’s an easier task.

Laying the favourite is the most common exchange strategy in greyhound racing. Favourites in six-runner races win roughly 30-35% of the time across the board. That means they lose 65-70% of the time. If you can identify situations where the favourite is overbet—perhaps benefiting from public name recognition, a misleading form line, or an unfavourable draw that the market hasn’t fully priced in—laying that favourite at short odds can be profitable. Your liability is limited by the short price, and you win more often than you lose.

Laying outsiders carries the opposite risk profile: you win frequently but face large payouts when the outsider defies the odds. Laying a dog at 10.0 means your liability is nine times the backer’s stake. One loss wipes out nine wins. This approach demands exceptional accuracy in identifying dogs that genuinely cannot win, and the margin for error is painfully thin. Most experienced exchange punters avoid laying at long odds on greyhound markets, where the randomness of six-dog racing on a tight track can produce shock results with uncomfortable regularity.

The sweet spot for laying tends to be in the mid-price range: dogs priced between 4.0 and 7.0. At these odds, the liability-to-stake ratio is manageable, the selections lose more often than they win, and the occasional payout against you doesn’t decimate accumulated profits. Selecting which mid-priced dogs to lay requires the same analytical rigour as selecting which to back—form, draw, grade, track conditions—applied with the opposite intent.

Exchange Strategies for Dog Racing

Trading—backing at one price and laying at another to lock in a profit—is the most sophisticated exchange strategy, and greyhound markets offer occasional windows for it. The approach relies on price movement. If you back a dog at 6.0 before the market shortens, then lay the same dog at 4.0 as money flows in, you’ve secured a guaranteed profit regardless of the result. The mathematics of the trade determine your exact return, which can be distributed evenly across all outcomes or weighted toward one result.

Greyhound markets move sharply in the minutes before a race, creating compressed trading windows. A dog that opens at 6.0 might contract to 4.0 in the final two minutes as kennel money arrives. If you’ve backed at 6.0, the lay opportunity appears rapidly and closes quickly. Successful trading requires being present and attentive at precisely the right moment—a demand that the frequency of greyhound racing, with races every ten to fifteen minutes across multiple meetings, makes both challenging and rewarding for those who can maintain focus.

Dutching—backing multiple selections to guarantee a profit regardless of which one wins—works on exchanges where you can set your own prices. If two dogs in a six-runner race are both available at prices that, combined, produce a return exceeding your total outlay, backing both creates a mathematical advantage. In practice, exchange markets rarely offer clean dutching opportunities on greyhounds because the back prices incorporate sufficient spread to eliminate easy arbitrage. But when markets are adjusting rapidly, temporary inefficiencies do appear.

The most reliable exchange strategy for greyhound racing is also the least exciting: use the exchange as an odds comparison tool. If the exchange back price exceeds the best bookmaker price, back through the exchange. If the bookmaker offers better, take the fixed-odds bet. This hybrid approach, combining exchange and traditional betting, consistently delivers better average odds than loyalty to either platform alone.

Commission and Its Impact on Returns

Commission is the exchange’s price for facilitating your bet. It applies to net winnings on a market, not to losing bets. If you win £100 on a greyhound race at Betfair’s standard 5% rate, £5 goes to the exchange and you pocket £95. Losses carry no commission charge. Over time, commission erodes returns in a similar way to the bookmaker’s overround, though typically by a smaller amount.

The actual impact depends on your trading pattern. Punters who place occasional large bets feel commission less acutely than high-frequency traders who churn through many small positions. A 5% charge on net winnings from a single evening bet is barely noticeable. The same 5% applied across dozens of small trades per week accumulates into a meaningful drag on returns. Calculate commission into your profit-and-loss tracking from day one to avoid discovering months later that your gross profit has been substantially reduced by the platform’s cut.

Betfair’s discount programme reduces commission for high-volume users, scaling down from the standard 5% based on the number of Betfair Points earned through betting activity. Smarkets’ flat 2% commission offers a simpler proposition: lower commission from the first bet, regardless of volume. For greyhound punters who trade regularly, the difference between 5% and 2% commission compounds significantly across a year’s betting. Maintaining accounts on both exchanges and directing trades to the lower-commission option—all else being equal—is a straightforward way to preserve more of your profits.

The Other Side of the Market

Betting exchanges didn’t replace bookmakers for greyhound racing, and they probably never will. The liquidity gap is too wide and the convenience difference too significant for most punters. But they offer something bookmakers categorically cannot: the ability to bet against a dog, to set your own price, and to trade positions before a race.

Those capabilities expand the punter’s toolkit in ways that reward analytical skill. If you can identify a dog likely to lose, an exchange lets you profit from that insight directly. If you can read pre-race market movement accurately, trading lets you capture value from price shifts that don’t require predicting the race outcome at all. These are fundamentally different skills from picking winners at the best available price, and developing them adds a dimension to your greyhound betting that fixed-odds markets alone cannot provide.

Start with small stakes, learn the interface, and treat your first month on an exchange as an education rather than a profit centre. The learning curve is steeper than placing a straightforward bet with a bookmaker, but the ceiling is higher for those willing to climb it.